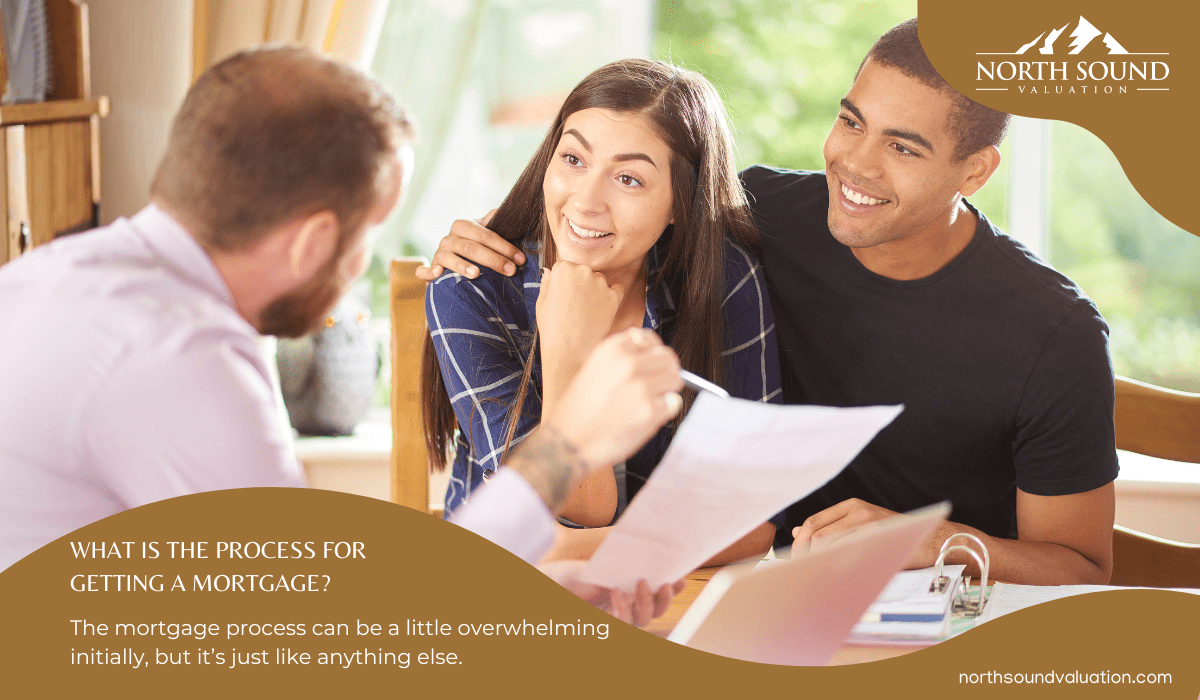

The mortgage process can be a little overwhelming initially, but it’s just like anything else. If you break down the tasks into steps, you’ll find that once you do it, you’ll have it figured out.

There is always help and professionals that will answer your questions. It just takes time and dedication.

At North Sound Valuation, we proudly provide expert residential property appraisals north of Seattle. We serve Snohomish, Island, and Skagit counties. Our experienced appraisers are ready to help you with your valuation needs, including home sales, estate planning, or pre-purchase evaluations.

Once you have found the home you want to buy, North Sound Valuation will provide you with the appropriate estimation of the house’s value.

If you are ready to buy a house in Snohomish (or the surrounding area) and need help getting a loan, take these six steps one at a time. You will get through the mortgage process just fine if you follow them.

Steps to take for a mortgage loan

- Get pre-approved.

- Shop for a house.

- Apply for a mortgage.

- Go through the underwriting process.

- Close

Get Pre-Approved.

Pre-approval is one of the most important steps in getting a mortgage. It means a financial institutionn has approved your ability to receive a certain amount of money, which you will use as leverage in negotiations with lenders. If you’re not pre-approved, your real estate agent will likely have to slow down the search process until you can get one.

Pre-approval allows for more flexibility during home shopping since buyers can make an offer on any property with their pre-approved funds.

Before you start looking for your new home, it’s important to know how much you can afford and how much house you can qualify for. To find out how much you can afford, contact several banks or credit unions ahead of time so they can determine what house price range may suit you best.

If you are applying for a mortgage, you may need proof of income (pay stubs) and tax returns from the past several years. If the new home you want costs more than expected, please ensure that your lender has enough room left in your budget.

The required documents vary depending on the type of mortgage you want and how much money you want to borrow. Generally speaking, however, here are some of the most important ones:

- Proof of income (pay stubs or tax returns)

- Documentation showing where your money comes from (bank statements)

- A list of assets such as retirement accounts and homes owned by other family members who may be co-signing on your loan

Once you’ve completed the pre-approval process, you’ll gather your application package together and submit everything back into one place where all parties can access it easily.

Now that you’re pre-approved, you can start shopping for a home.

Now that you’re pre-approved, you can start shopping for a home. You can shop with confidence and know exactly what your budget is. You also have a better idea of what you want: whether it be a condo in the city or a house in the suburbs, knowing how much money you have to spend will help narrow your search.

Apply for a mortgage.

Once you find the perfect home, we’ll gather the documents we need to process your loan application. Your mortgage professional will help guide you through this process and ensure everything is adequate.

The required documents vary depending on the type of mortgage you want and how much money you want to borrow. Generally speaking, however, here are some of the most important ones:

- Proof of income (pay stubs or tax returns)

- Documentation showing where your money comes from (bank statements)

- A list of assets such as retirement accounts and homes owned by other family members who may be co-signing on your loan

Check to see if you qualify for any of these mortgage programs.

If you’re considering buying a home, several different types of loans are available. Each loan type has its requirements, so it’s important to understand how each works before deciding which one is right for you. Here are some of the most common types:

- Government loans—If your income falls within certain limits, you may be eligible for a government-backed mortgage. These loans include FHA and VA mortgages (for active duty military members). Government loans typically offer lower interest rates than other options and may require less money down—but they also have more strict qualification standards than those on the private market.

- Conventional mortgage—This is what most people think about when they think about getting approved for a loan; banks or other lenders offer it without any government backing. Conventional mortgages tend to have higher rates than their federal counterparts but can still be relatively affordable compared with other types of financing like auto or student loans.

- FHA loan—An FHA loan stands apart from conventional ones because it allows borrowers who don’t meet traditional criteria (like having at least 20% down) to qualify for financing through insurance provided by HUD (the Department of Housing and Urban Development). The downside? Borrowers who use this program often pay higher interest rates to offset losses that could occur if someone defaults on their monthly payments after obtaining an FHA-backed mortgage.

Next, your loan will go through the underwriting process.

Once you’ve gone through the application process, your loan will go through the underwriting process. Underwriting is reviewing your financial information and verifying that you can repay the loan.

Your loan officer will review your application to ensure all the information is correct before sending it for approval by an underwriter. The underwriter will review this information to ensure it’s accurate and complete. They’ll ensure there aren’t any issues with your credit history or income (if applicable). They’ll also want to verify that you can repay this loan over time per their guidelines.

Once the underwriter has approved your loan, they’ll send it back to the loan officer. At this point, you’ll have a decision from the lender — whether they approve or deny your application. If they deny you, then there’s nothing more that can be done. However, if they approve your loan, then congratulations! You’re ready to start closing on your home purchase!

Closing

The closing process is a milestone in any home purchase, as it’s when you and your mortgage lender finally take ownership of the property. One of the first steps in the closing process includes the home’s appraisal. The transaction proceeds if the appraisal arrives at or above the contract price. If the appraisal falls below the contract price, the transaction will pause until the buyer and seller negotiate a new price.

During closing, you’ll be required to pay closing costs, including an appraisal fee (usually $300–$500), title search fees ($225–$400), and other fees related to the mortgage lender’s underwriting process. These fees vary from one lender to another but are typically around 2% of the loan amount.

- Don’t feel daunted by the mortgage process; just make sure you understand each step as it comes along.

- Even if you do get overwhelmed, owning a home is worth it.

- Don’t be afraid to ask questions and say no to things you don’t want.

- If something seems too complicated or confusing, ask for help!

Buying a home is exciting, and we hope you’ve enjoyed learning about the mortgage process. We understand that it can sometimes seem daunting, but if you take it step by step, you will feel more confident about the process.